GBST’s Head of Product, Andy Boniface, discusses how six years after the pensions freedoms legislation was enacted, advisers continue to struggle to access the full range of flexibility for their clients through mainstream platforms.

GBST’s Head of Product, Andy Boniface, discusses how six years after the pensions freedoms legislation was enacted, advisers continue to struggle to access the full range of flexibility for their clients through mainstream platforms.

When the pension freedoms legislation was enacted in April 2015, it removed many restrictions around defined contribution (DC) schemes and provided more flexible access to pension savings. Although the rules allowed for a wider range of income options, six years on advisers continue to struggle to access the full range of flexibility for their clients through mainstream platforms.

Even though savings in pensions wrappers account for half their assets, advised platforms generally remain focused on accumulating money, rather than providing a choice of decumulation options. While some specialist ‘at retirement’ providers have an abundance of withdrawal functionality and can offer advisers and clients significant control over scheduled and ad hoc income payments, along with the flexibility to blend pension investments, drawdown, guaranteed income, and to alter the combination as required, most mainstream platforms do not provide these capabilities and flexibility.

An analysis of 26 advised platforms conducted by the lang cat found that seven currently offer less than half of the 14 pension income functions listed, which include flexi-access drawdown, drip-feed drawdown, and portfolios designed for drawdown and guaranteed income products. Basic functionality including an uncrystallised fund pension lump sum (UFPLS) was missing from one platform, while five did not include natural income options. Only 13 of the platforms analysed offered consolidated income payments, while just nine provided tax-efficient withdrawal tools, and only four included guaranteed income products. The technology exists to support the full list of functions, and while five platforms include 11 of them, and three offer 12, no single platform provides all 14 as part of their proposition.

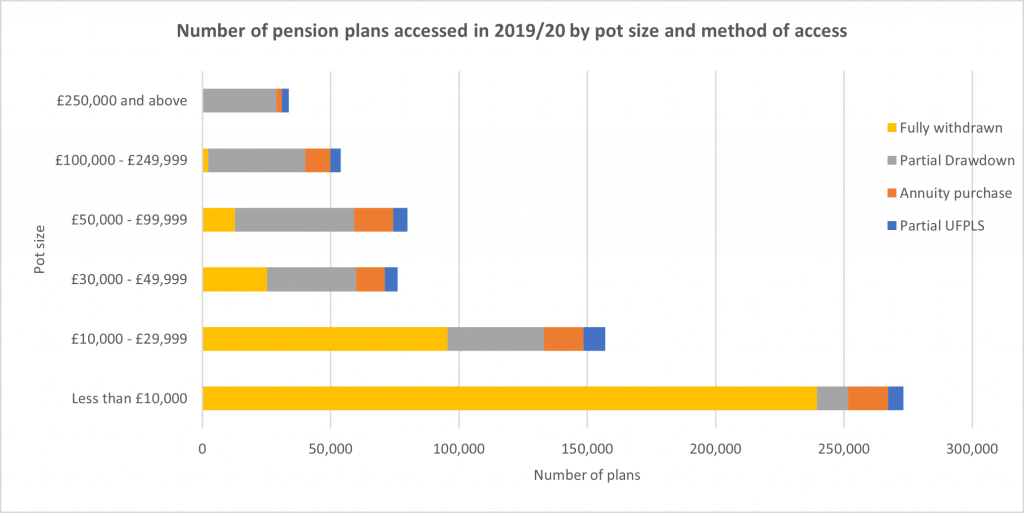

Yet the need for pension flexibility is here to stay. According to HMRC, the total value of flexible withdrawals from pensions since pension freedoms were introduced in 2015 has now exceeded £45 billion (1). The latest FCA retirement income data showed that in the year to March 2020, 674,000 pension pots were accessed for the first time, with over half of these plans completely withdrawn, almost one-third in partial drawdown, and one in ten used to purchase an annuity (2).

Source: FCA retirement income data 2020

While the overall impact of Covid-19 on retirement decisions is not yet fully understood, the Office for National Statistics (ONS) recently reported that in the three months leading up to February 2021, employees aged 50 and over were more likely to be working fewer hours than usual in comparison to those aged under 50 years. The number of hours was reduced even further for those aged over 65. The report also found that a quarter (1.3 million) of those on furlough are 50 and over, with almost a third of these workers saying there is more than a 50% chance that they will lose their job when the scheme ends. The ONS observes that older people who lose their jobs face a higher risk of long-term unemployment than younger people (3). This suggests that many of these older workers may never return to employment, or at least not to a level of salary that enables them to continue accumulating retirement funds to meet planned objectives without the need to access their pension income earlier than expected.

Even without considering the short- and long-term effects of Coronavirus, people’s plans for retirement do not always stay on track. Research by Just Group earlier this year found that nearly half (47%) of retired over-55s had stopped working earlier than they expected, with 33% citing ill health, 15% for redundancy, and 8% to care for a family member (4).

Some providers do recognise the need to personalise the ‘at retirement’ experience. Canada Life, for instance, can provide flexibility for the retiree to easily adjust their income choices based on evolving lifestyle and later life care needs utilising full, partial or phased drawdown options. The individual can make additional contributions to the pension pot or withdraw at any time while continuing to receive income from the fund investment, they can set a level of guaranteed income and any money remaining in their pension pot can be passed onto beneficiaries at death. However, most mainstream platforms are a long way off delivering this level of flexibility.

As longevity, employment patterns, and retirement journeys change, flexible access to pensions will become increasingly important. People will need blended solutions that combine different types of investments and retirement products to meet a range of requirements. Income planning for later life is no longer just about retirement day. Those accessing their pensions today are likely to face multiple financial demands as they grow older. This may include the need to withdraw ad hoc funds to help children or finance other one-off expenses. The security of a guaranteed income might become appealing to cover fixed costs in the future, complemented with the option to continue growing investments and potentially leave a legacy behind.

Qualitative research into decumulation journeys published in October last year by the Department of Work and Pensions, found, as you would expect, that decisions about whether or how to access a pension pot differ from person to person. The report stated: “Whether an individual went ahead with accessing their pot(s), and in what way, depended on a complex interaction between their circumstances, personal beliefs, values, and capabilities. This included how they viewed their potential life expectancy and years of independent retirement, their attitudes to financial risk, trust in financial institutions, preferences for supporting adult children, proximity to planned retirement age, health and employment status, perceived financial capability and, where applicable, how they took their partner’s plans into account (5).”

Retirement is now a deeply personal journey, with the need for almost as many different plans as there are pensioners. The recent ONS population statistics tell us that in 2019, 4.66 million people in the UK were aged between 50 and 54, the most of any age group. By 2050, it is projected that a quarter of the UK population will be aged 65 years and over, up from approximately one-fifth in 2019 (6). Over the next three decades, the number of people planning for retirement will increase dramatically. By not taking advantage of the ‘at retirement’ capabilities available to them to deliver pension freedoms as intended, mainstream platforms risk a significant amount of assets simply walking out the door as customers reach retirement age.

The pension freedom rules promised greater control and flexibility over how we fund our retirements, but six years on, many platforms are still falling short of delivering that promise. The technology is available and specialist providers are leading the way with what can be done. Lagging platforms will need to catch up and provide a wider range of functionality to support advisers and their clients through complex ‘at retirement’ options. Otherwise, they risk seeing a large proportion of their pension assets disappear as people seek decumulation flexibility elsewhere.

For more information about GBST’s retirement planning solutions can be found here.

SOURCES

(1) Flexible payments from pensions (Gov.uk)

(2) Retirement income market data 2019/20 (FCA)

(3) Living longer: Older workers during the coronavirus (COVID-19) pandemic (Office for National Statistics)

(4) Nearly half of early retirees forced out of work by poor health or redundancy, Just Group research reveals (Just)

(5) Pension Freedoms: a qualitative research study of individuals’ decumulation journeys (Gov.uk)

(6) Overview of the UK population: January 2021 (Office for National Statistics)

Posted in: Wealth Management Administration